They get a foul identify due to their short-term nature, however at their core, they’re simply choices with a shorter lifespan. The entire similar ideas of choices apply to them, so if you may get previous the stigma related to them, there are many buying and selling alternatives current. As Euan Sinclair as soon as stated about this topic, “the house cat and tiger have more similarities than differences.”

And by the way in which, for these associating weekly choices with playing, it is best to know that the majority main monetary establishments these days are important gamers in weeklies. Simply ask Roni Israelov, the previous supervisor of choices methods at AQR, who informed the FT, “If I have monthly options, I get 12 independent bets per year. If I have weekly, I get 52 bets per year. Daily gives me 252. If you’re generating trading strategies, the ability to have more ‘at bats’ and more diversification by taking more independent trades can be useful.”

Elevated Capital Turnover

Suppose you are a mechanical choices dealer who routinely sells choices in 45-60 DTE expirations with excessive implied volatilities. Take your earnings at 50% of max revenue. And you would maintain your common commerce for a number of weeks earlier than reaching your required revenue stage.

If we take the identical assumptions however with shorter, 10-15 day expirations, you may be holding your common commerce for just some days.

You are turning over your capital a number of instances faster, and assuming you may choose trades with an analogous anticipated worth, you are capable of generate larger returns, rising your pattern measurement and, in idea, lowering the variance of your portfolio.

I am simplifying in an enormous approach. Quick-dated choices have completely different properties within the type of market dynamics and Greeks that’ll have an effect on this equation significantly.

Nevertheless, the idea is that getting extra “at-bats,” to make use of Israelov’s phrase from the intro of this piece, is usually higher, assuming you may preserve the remainder of the variables comparatively fixed.

Volatility is Extra… Unstable in Weekly Choices (“Vol-of-Vol”)

As a precept, shorter-dated (i.e., weekly choices) have much less vega than longer-dated choices. To notice, vega is an possibility’s sensitivity to modifications in implied volatility. Identical to delta, theta, and gamma, the results of an possibility’s vega are simple to calculate. For every one-point improve in implied volatility, the choice worth ought to change by its vega.

For example, let’s take an SPX name possibility price $10.00 with an implied volatility of 18 and a vega of .20. Ought to the implied volatility of the probabilities improve to 19, the choice’s worth would improve to $10.20. This works in each instructions.

As a result of short-dated choices sometimes have low vega, many merchants mistakenly assume that weekly choices are comparatively unaffected by vega, i.e., the danger of implied volatility rising or lowering.

However that will be incorrect. Whereas short-dated choices have low vega on the face, the implied volatility on short-dated potentialities is far more risky. In different phrases, volatility is extra… risky.

The results of short-term volatility dampen with time. With out referencing precise numbers, take into consideration the distinction in how the worth of a 1-year LEAP and a 1-day weekly possibility would reply to a ten% change within the underlying worth. Certain, each values are affected, however with an entire yr till expiration, that 10% one-day change is sort of a blip on the radar so far as the place the underlying might be a yr out.

So short-term implied volatility must account not just for these “black swan” kind dangers but in addition for business-as-usual, which is realized volatility being under implied.

The sellers of those choices aren’t naive and have to be compensated for taking over this big selection of dangers, so that they demand the next variance premium.

So this property of short-dated choices can each assist and hurt you, relying on which aspect of the commerce you’re on and what kind of dangers you favor to take.

Volatility is Generally Too Excessive (Or Low)

Within the earlier part, we mentioned how the implied volatility on short-dated choices is extra risky than the IVs on longer-dated choices. It is because, with so little time to expiration, a slight short-term aberration like order move or a chunk of reports can dramatically have an effect on the place the underlying trades are at expiration. With extra time to expiration, these components kind themselves and volatility tends to stay nearer to a longer-term common

With volatility being extra risky in these choices, you may generally establish durations through which the market overreacts and also you deem volatility too excessive or low, permitting you to swoop in and make a very good commerce rapidly.

Theta Decay is Totally different in Weekly Choices

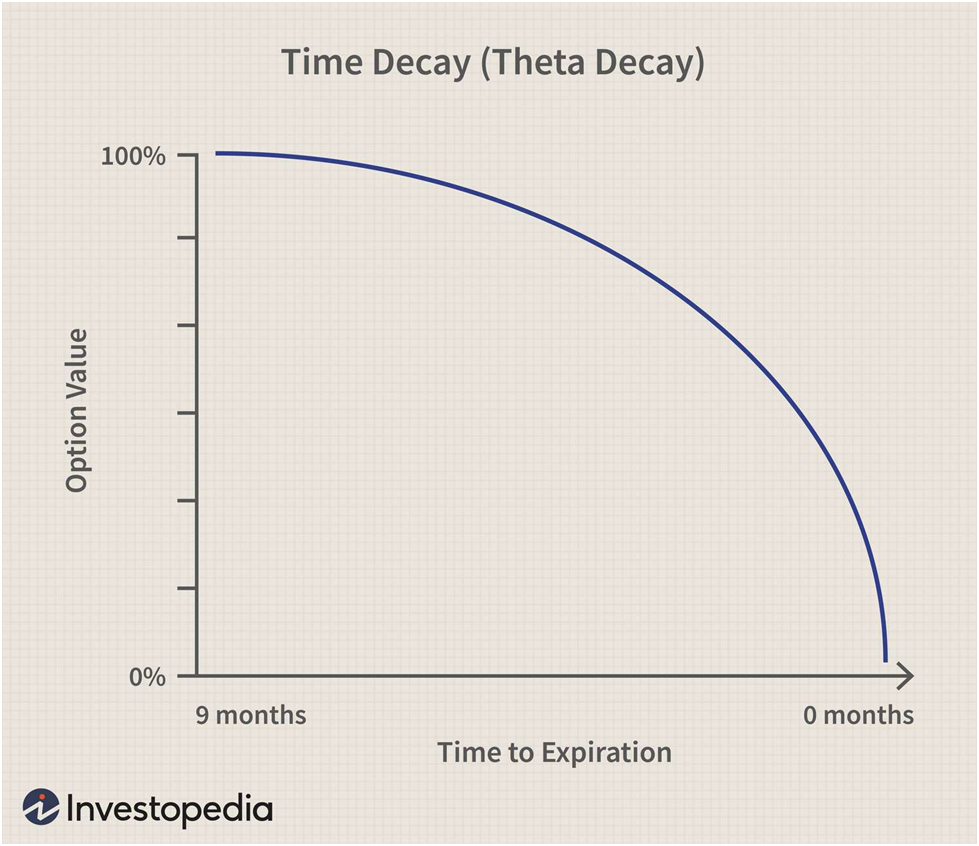

Longer-dated choices profit from considerably optimistic theta, giving a dealer who sells longer-dated choices a optimistic carry from theta decay. All through the lifetime of the choice, theta decay happens at a non-linear fee. This is a chart for an intuitive sense:

Probably the most widespread arguments in favor of longer-dated choices, particularly within the vary of 30-45 days to expiration, is that these choices not solely have a lot theta, however they’re proper on the candy spot the place the speed of theta decay begins to speed up. Certainly a powerful argument.

And proponents of this philosophy are proper. Absolutely the stage of theta for longer-dated choices is certainly larger. The theta decay per day as a proportion of the choice worth is way larger in shorter-dated choices.

Let’s evaluate the identical strike in two completely different expirations. A $SPY .30 delta name expiring in 5 days is buying and selling for $1.21 with a theta of -0.21, representing a -17% fee of decay day by day, whereas a .32 delta name expiring in 37 days is buying and selling for $4.10 with a theta of -0.11, which is a -2.61% fee of day by day decay. After all, the speed of theta decay will speed up within the longer-dated possibility as expiration nears.

So you could have two choices, each of that are inherently right. You’ll be able to go along with the longer-dated possibility on the “sweet spot” of the theta decay curve and experience it for a number of weeks, or you may churn and burn weekly choices, turning your capital over and transferring on from trades in a short time.

Weekly Choices Have Very Excessive Gamma

In the event you recall, gamma is the speed of change of delta. The upper the gamma, the extra dramatically a tick within the underlying will have an effect on the delta. As a rule, the nearer choices get to expiration, the upper their gamma is, particularly for near-the-money choices.

However why is that this? As expiration nears, choices that are not within the cash expire nugatory. This makes the worth of near-the-money choices extremely suspect and topic to huge worth swings, which is the intuitive definition of gamma.

There’s an elevated uncertainty as to which choices will expire nugatory, so every tick within the underlying creates extra important swings within the delta as you get nearer to expiration.

This can be a reward and a curse. In the event you’re on the correct aspect of the market, you see important features rapidly, however getting caught on the opposite aspect means your fortune rapidly wanes.

Backside Line

Weekly choices to month-to-month choices as day buying and selling are swing buying and selling. Fortunes are gained and misplaced extra quickly in weekly choices, they usually favor the bolder, faster-acting dealer over the analytical “dot the i’s and cross the t’s” kind of dealer.

Loads of profitable merchants commerce weekly choices, people who commerce longer-dated choices, and many who commerce each. Choices buying and selling could be very a lot about trade-offs, and stated trade-offs typically come all the way down to temperament or private choice.

One certain factor is that if you happen to commerce weekly choices, you must grow to be far more lively as a dealer, which is a price in itself.

Associated articles: